Udanchoo is a Hindi word meaning – to fly away or disappear. I wanted to use it for a bit of wordplay - thought it rhymes with Yahoo - and its meaning aptly captures the theme of this blog.

Background

“Looking ahead, our Q4 outlook, which Ken will return to later, is not indicative of the performance we want. While there are some well-known headwinds year-over-year, and even quarter-over-quarter, like the loss of the Alibaba TIPLA, we are also experiencing continued revenue headwinds in our core business, especially in the legacy portions.” - Marissa Mayer - Yahoo! Inc. – CEO in Q3 2015 Earnings Call

The above quote from Marissa Mayer euphemistically describes the situation at Yahoo, which can be summed up more directly as follows - The Outlook for the current proposed course is bleak at best. Yahoo is facing challenges at a number of levels:

The following are the key take-away from the above tables:

Background

The key points to note are as follows:

Notes & Assumptions

Background

“Looking ahead, our Q4 outlook, which Ken will return to later, is not indicative of the performance we want. While there are some well-known headwinds year-over-year, and even quarter-over-quarter, like the loss of the Alibaba TIPLA, we are also experiencing continued revenue headwinds in our core business, especially in the legacy portions.” - Marissa Mayer - Yahoo! Inc. – CEO in Q3 2015 Earnings Call

The above quote from Marissa Mayer euphemistically describes the situation at Yahoo, which can be summed up more directly as follows - The Outlook for the current proposed course is bleak at best. Yahoo is facing challenges at a number of levels:

- the stock has fallen c. 35% this year;

- Yahoo’s Core Business - Internet search, communication and digital content – is facing significant headwinds, with both profitability and free cash flows at an all time low;

- leadership is facing a crisis – the new leadership, which was put in place in 2012, seems to be fighting a losing battle to turn things around; staff morale is at an all time low; staff turnover is at an all time high – Yahoo is bleeding talent and senior staff at an alarming rate; for company whose main competitor is Google, this is a very bad place to in (this Forbes article nicely sums up the current state of affairs at the company - http://www.forbes.com/sites/miguelhelft/2015/11/19/the-last-days-of-marissa-mayer/);

- managements next big step to unlock value – spinning of Yahoo’s 15.4% Alibaba stake – presents significant risk of eroding value, instead of creating it; and,

- Starboard Value, an activities investor, has all but issued an open threat to the leadership to change course, or face a proxy fight for board seats (http://www.starboardvalue.com/publications/Starboard_Value_LP_Letter_to_YHOO_08.10.15.pdf).

- Finally, I think this is a very good article on Yahoo's rise and fall - http://www.wired.com/2015/11/

once-upon-a-time-yahoo-was- the-most-important-internet- company/

Neither status quo, nor the management proposed action to spin-off Alibaba create value for shareholders or the company

Yahoo also has a tremendous opportunity to create value for its shareholders. In particular, my analysis concludes that Yahoo could take the following actions to significantly change Market’s view of what it’s worth, and unlock value for its shareholders:

- Drop its proposed spin-off of its 15.4% Alibaba stake; this action has some significant downside risks attached which far outweigh the positives;

- Sell its Core Business, distribute the proceeds (including existing cash) to shareholders, and end up becoming a pure holding company of its Alibaba and Yahoo Japan stakes.

My analysis shows that pursuing the above action produces an intrinsic value per share of at least $47.5; the shares closed at $33.11 @20 November 2015, implying a discount of 30% to intrinsic value.

In my view, neither status quo, nor the spin-off of Alibaba should be chosen, I believe that the market will continue to apply a significant discount to intrinsic value under either scenarios. This is mainly due the market, rightly in my opinion, being concerned with the following trends:

Core Business trend

- Yahoo has burnt c. $550m of cash in the last 3 years trying to turn around its Core Business; in spite of the spend, EBITDA has fallen by 35% and free cash flows by c. 24% during this period.

- A significant amount of cash – c. $550m - has been wasted in the last 3-4 years on acquisitions which have not performed to expectations (in many cases, they have resulted in a complete write-off). The market is rightly concerned of this trend continuing.

- In addition, Yahoo has lost a significant revenue stream last year, with the end of its licence revenue from Alibaba. The Alibaba license revenue contributed c $170m per annum.

- The Core Business continues to face significant headwinds as competitors eat into Yahoo’s market share, and it continua's to loose talent at an alarming rate.

Tax risk on the proposed Alibaba spin-off

- The tax risk under the Alibaba spin-off option has increased significantly after IRS’ refused to provide a ruling confirming tax free status

- This adds a lot of uncertainty to the transaction – the risk of an IRS challenge in future, and the potential duration of the risk – 5-10 years - will mean that, even in a best case scenario, value remains trapped for a long period; and, in a worst case scenario, value is wiped out.

- Per my calculations, the down-side to the Alibaba spin-off is could be as high as 70% (c $22bln) of the value of Yahoo’s Alibaba stake; whereas, the upside is not significantly different to the alternative course – i.e., not undertaking the spin-off and selling the Core Business instead.

Current structure & Market’s view

In order to understand the current situation with Yahoo, it is helpful to summarize the current structure; look at market’s view of the value, and see what premium or discount the market is applying to Yahoo’s current proposed course (i.e., spinning off the Alibaba stake, and investing to turnaround its Core Business).

As can be seen from the current structure, Yahoo Inc. has three main assets:

- The 15.4% interest in Alibaba - a leading, China based, provider of online and mobile marketplaces in retail and wholesale trade, as well as cloud computing and other services;

- The 35.5% interest in Yahoo Japan – a leading Japan based provider of internet search, information listing, communication & contect, and e-commerce services; and,

- The Yahoo’s operating business (“Core Business”) - principally based in US, and engaged in providing Internet search, communication, and digital content.

It is worth looking how the Market views the various component parts, and the resulting implied premium or discount applied by Market to Yahoo Inc’s shares. The below tables summarise the position (based on share price at 20 November 2015, and information from Yahoo Inc’s Q3 financials).

The following are the key take-away from the above tables:

- The first table shows that Yahoo Inc’s Market Cap ($ 31.3bln) is less than Yahoo Inc’s share of Alibaba & Yahoo Japan Market Cap ($ 38.96 bln);

- The second table shows that the Market is applying a c. $12.3bln discount to Yahoo Inc, when compared with Yahoo Inc’s non-core asset (mainly its cash balance, and Alibaba and Yahoo Japan stake).

In order to check if the c. $12.3bln discount applied by the Market is correct, one needs to break down the values into the following component parts

| |

I have summarized my intrinsic value estimates for the various component parts in the table below (this is before the estimated tax liability on a Alibaba spin-off)

|

Key points of note re intrinsic value estimates

- I have calculated the intrinsic value of the operating assets using a DCF method, with source information from company financials (please see at appendix for the intrinsic value calculation for Alibaba, Yahoo Japan, and Yahoo’s Core Business).

- The debt, cash, and non-operating assets have been taken from the most recent earnings reports available.

- I have applied a 2% discount to Alibaba and Yahoo Japan’s intrinsic value to account for the fact Yahoo Inc’s stake is trapped inside a corporate structure and cannot easily be crystallised. In the Yahoo Inc Consolidated column, I have added up the net value of equity based on Yahoo Inc’s share of equity (15.4% for Alibaba, 35.5% for Yahoo Japan, and 100% for the Core Business).

- The value of employee stock options has been calculated using information available from the company financials, and using Black Scholes method.

- In conclusion – my value of intrinsic value for the Alibaba and Yahoo Japan business is comparable with the Market Cap for those business; and, after adding Yahoo’s Core Business value, it appears that the market is pricing a 32% discount to intrinsic value. This discount needs to be compared with the estimated tax liability in order to identify any mispricing in the Market.

Alibaba spin-off – estimated tax liability

Background

- With a view to unlocking value in its Alibaba stake, in January 2015, Yahoo announced a plan for a spin-off the its remaining holdings in Alibaba into a newly formed company - Aabaco Holdings, Inc. (“Aabaco”). In addition to transferring the Alibaba stake, Yahoo will also transfer 100% ownership of its Small Business Unit, which helps small businesses get websites off the ground and sell things online. Under the spin-off the stock of Aabaco will be distributed pro rata to Yahoo stockholders, resulting in Aabaco becoming a separate publicly traded registered investment company.

- Following the completion of the transaction, Aabaco will own all of Yahoo’s 15.4% interest in Alibaba, and a 100 percent ownership interest in Aabaco Small Business, LLC, a newly formed entity which will own Yahoo Small Business. The transaction is expected to be tax free under the US tax rules, however, for certainty, Yahoo decided request a private letter ruling from the IRS confirming that the spin-off was to be tax free.

The below show’s the planned spin-off structure at a high level.

Tax status of the spin-off

In order for a spin-off to qualify as tax-free to both the parent and its shareholders for U.S. federal income tax purposes, it must qualify under Section 355 of the Internal Revenue Code. See this link for reference - http://www.wlrk.com/files/2013/SpinOffGuide.pdf

Broadly, Section 355 requires the following conditions to be met in order for the Spin-off to qualify as tax free:

- The parent must give up control of the spin-off company (generally, stock representing 80% of the voting power and 80% of each non-voting class of stock). In Yahoo’s case, it will give up 100% of Aabaco.

- Immediately after the spin-off each of the parent and the spinoff company must be engaged in an “active trade or business” that was actively conducted throughout the five-year period before the spin-off. Yahoo’s plan to transfer its Small Business Unit to Aabaco is aimed at this condition.

- The spin-off must have a valid business purpose; in particular, its real and substantial purpose should be non-tax motivated. Yahoo in its filings has stated that the transaction has strong business purpose (although, it is difficult to see how tax will not be a key driver)

- If one or more persons acquire a 50 percent or greater interest in parent or Spin-off company within two years of the spin-off, then the gain on Spin-off will be taxable for parent. This means that neither Yahoo Inc, nor Aabaco, can be acquired by a third party for 2 years post spin-off.

Overall, it would appear that the proposed spin-off of Aabaco should be tax free under current rules. But a major roadblock arose when the IRS refused to rule on the tax free status of the spin-off; the IRS did not say whether it thought the transaction was taxable, it simply refused to opine.

Alibaba spin-off – estimated tax liability

According to a report from Bloomberg News in May 2015, when the IRS responded:

Isaac Zimbalist, senior technician reviewer at the IRS’s Office of Associate Chief Counsel (Corporate), said on Tuesday the government agency is considering changes to rules concerning spinoffs. "The issue comes down to whether we’ve dropped a hot dog stand or a lemonade stand into a business that is primarily publicly traded stocks, cash and other wonderful things that I call appreciated property," Zimbalist said.

I have highlighted the relevant quote for Yahoo’s proposed spin-off above. Broadly, my reading of this is that, the assets the Spin-off Co relies on to satisfy the "five-year active trade or business" requirement of the tax-free spin-off rules need to be a meaningful proportion of its total assets – i.e., in Yahoo’s case, its Small Business Unit needs to be a meaningful piece of the overall value. As the new rules have not yet been formulated, it is difficult to say what the IRS means by “a hot dog stand or a lemonade stand into a business that is primarily publicly traded stocks.” But taking a guess – Alibaba is roughly worth $ 30bln, and I would be surprised if the Small Business Unit that it proposes to transfer is worth more than 1% of the Alibaba value. Anyway, all this in itself is not a deal killer for Yahoo – the IRS has indicated in a public statement that any future guidance issued as part of the rule changes would not apply retroactively to transactions completed prior to the issuance of such guidance. But, that in itself doesn’t mean that the IRS cannot challenge a transaction. The whole purpose of getting a private letter ruling is to remove the risk of a future challenge – in effective, being able to unlock full value by eliminating a cash tax risk down the line. Nevertheless, all this adds to the uncertainty, and increases the downside risk significantly. The main areas of concern are as follows:

- As part of the spin-off arrangement, Aabaco has indemnified Yahoo Inc with respect to any future tax liability. Therefore, it is Aabaco’s shareholders who are on the hook for any future tax bill. This means that Aabaco will continue to trade at a significant discount – equal to future value of the estimated tax risk, for the duration that the risk exists.

- Yahoo plans to complete the spin-off in January 2016. This means that it will be required to include the transaction in its 2016 tax return that will be due 2017. The IRS then has a three year window of enquiry. Therefore, one won’t know until the end of 2020 if the tax risk has fallen away. And in the worst case scenario, where the IRS decided to open an audit, things could get ugly – e.g. considering the quantum of taxes at stake, the company will most likely engage in a protracted legal process. Therefore, for Aabacus shareholders, the risk could persist for 5-10 years.

Overall, even though the proposed spin-off should qualify as a tax free transaction under current rules, the IRS’ stance lately has increased the downside risk. But, the bigger risk for the shareholders is that the uncertainty created by not having the tax ruling, combined with the fact that Aabacus will be on the hook for any future tax bill, defects the purpose of the spin-off – i.e., to unlock value in the Alibaba shares.

Finally, in addition to the US tax risk, the Chinese tax authorities have issued a bulletin in February 2015 which states that indirect transfers of PRC taxable property, which includes equity interests in PRC resident enterprises, by a foreign company could be subject to a 10% withholding tax if the transaction does not have a reasonable commercial purpose. Although Yahoo has stated in its filings that it believes this new bulletin should not apply to the proposed spin-off, it does add more uncertainty to the transaction.

In the table below, I have calculated the

likely tax liability under the various scenarios

The key points to note are as follows:

- Intrinsic value includes a 2% discount for the fact that Aabaco’s Alibaba stake will trade at a discount to Alibaba’s quoted shares because it cannot be unlocked at least for 2 years

- The cost base used to calculate the taxable gain is based on Yahoo Inc’s financials

- In addition to the 40% tax on gain (35% federal, plus 5% for state taxes), I have assumed that any indemnity payment to Yahoo by Aabaco will itself be taxable; therefore, I have included a gross up payment from Aabaco to Yahoo to cover the additional taxes.

- The PRC withtholding tax @10% is calculated on the gross value – i.e., assumes no benefit for cost base.

- The probability weights for each scenario is my subjective assumption. Although the transaction should be viewed as tax free under current rules, the increased uncertainty triggered by no ruling, IRS’ proposed rule changes, and the lengthy duration of the risk, merit these probability weights.

The table below I have calculated the after tax intrinsic value for Yahoo Inc post a spin-off

| |||

The key points to note are as follows:

- The uncertainty – i.e., probability weighted estimate – produces an intrinsic value that is not significantly different to the current Yahoo Inc share price of $33.11

- Although the upside scenario – no tax - means that the current price is c32% below intrinsic value, the down-side scenario – full tax - produces an equally damaging effect where current price could be c29% above intrinsic value.

- In conclusion, the uncertainty and risk of permanent capital loss should mean that the spin-off is not the best option in front of Yahoo.

Alternative scenario - Sell Core Business

- The proposed alternative scenario, where Yahoo sells its Core Business, and continues to hold its interest in Alibaba and Yahoo Japan, creates significant value for the shareholders.

- Yahoo’s Core Business should be of interest to a number of competitors, and potentially financial buyers – it has a number of unique users, significant search revenue, strong brand recognition, and valuable intellectual property.

- Post the sale of the Core Business, Yahoo Inc will end up as a passive holding company for its 15.4% and 35.5% interest in Alibaba and Yahoo Japan respective. It could either continue to hold this stake, or be eventually sold. It is worth noting that either one of Alibaba, Yahoo Japan, or Soft bank could be motivated to acquire this stake. Softbank is the largest shareholder in both Alibaba (where it holds c32% interest) and Yahoo Japan (where it holds a 43% interest). It would make a lot of sense for Softbank to consolidate its holdings by acquiring Yahoo Inc post the sale of the Core Business. This article I found online throws out some very interesting possibilities in this regard (http://blogs.wsj.com/japanrealtime/2015/01/26/mayers-yahoo-plan-could-affect-softbank-interests/)

The table below calculates the likely tax liability on the sale of Core Business

Finally, in the below table I have shown the after tax intrinsic value for Yahoo Inc post a sale

of the Core Business

The key points to note are as follows:

- The after tax intrinsic value equates to c. $47.5 per share, implying a 30% premium to the $33.11 share price at 20 November 2015.

- The value capture is more or less similar to the best case scenario under the Spin-off option, with the added advantage of no uncertainty.

In Conclusion

- Yahoo should drop its pursuit of Alibaba spin-off and pursue a strategy of selling its Core Business.

- This revised strategy has the potential to significantly unlock value for shareholders both in the near term, and down the line.

Afterword

I was inspired to research the situation at Yahoo by something I read in Security Analysis, a 1940 classic written by none other than Benjamin Graham and David Dodd, and an absolute must have reference for a student of value investing. In the book is a description of a risk free trade implemented by Ben Graham. The Du Pont Corporation, which controlled huge assets and dominated more than a handful of industries, had used its surplus cash to acquire a large block of GM stock. Despite these holdings, Du Pont traded at the market value that only equated the value of its GM stake. Graham noticed this mispricing in the market and reasoned that either the market was overvaluing the GM shares or it was ignoring the worth of Du Pont’s own operations.

Most investors in this situation would have been happy to simply go long Du Pont, and wait for the Market to correct its mispricing. But not Graham; he implemented an ingenious risk-free trade by going long Du Pont shares and simultaneously selling short an equivalent value in General Motors shares. The market soon vindicated Graham as Du Pont’s share price soared. Graham sold his Du Pont shares and closed out the short position in GM – pocketing a risk-free return.

Alibaba – Intrinsic value estimate using DCF

Notes & Assumptions

- Base year information is based on Alibaba earnings June 15 earnings report.

- As always, for a high growth business that is Alibaba, I have been conservative in my revenue growth assumptions – Alibaba has grown revenues by close to 60% CAGR over the last 4 years, and 45% in the last year; I have assumed revenue growth stays at 25% over the next 5 years, and drop’s off evenly to 2.4% in year 10. China retail is projected to grow at 25% over the next 5 years.

- Similarly, for EBIT margin, I have assumed that it starts off at the current year margin of c45%, but drops off evenly to 40% in year 10. The business has strong operational leverage.

- I have assumed a WACC of 8.58%, calculated using the company’s capital structure, and per CAPM

- The value of employee share options have been calculated using Black Scholes formula. The source data on number of options, weighted average strike price, and volatility is from company financials.

- In conclusion, my estimate of intrinsic value broadly equates to current market cap of Alibaba.

Yahoo Japan – Intrinsic value estimate using DCF

Notes & Assumptions

- Base year information is based on Yahoo Japan’s September 15 earnings report.

- Yahoo Japan is a mature business with strong cash flows, operational leverage, and solid margins. I has grown revenues at 8% CAGR over the last 5 years. I have assumed a 7% revenue growth rate for the next 5 years, dropping off evenly to 0.61% (the long term Japan growth rate) in year 10.

- EBIT margin, has averaged 5% over the last 5 years, with the most recent year’s email being 42%. I have assumed a EBIT margin of 41% for year 1, dropping off evenly to 40% in year 10.

- I have assumed a WACC of 6.79%, calculated using the company’s capital structure, and per CAPM. Being a mature, stable business based in Japan, it merit’s a lower WACC when compared to Alibaba.

- The value of employee share options have been calculated using Black Scholes formula. The source data on number of options, weighted average strike price, and volatility is from company financials.

- In conclusion, my estimate of intrinsic value broadly equates to current market cap of Yahoo Japan.

Yahoo Core Business

Notes & Assumptions

- Due to the significant headwinds and volatility in Yahoo’s Core Business, I have calculated intrinsic value using 3 possible scenarios as follows:

- Base Case: Free cash flow drops significantly over the next 3 years, but grows and stabilises thereafter.

- Worst Case: The business continues to bleed cash and is worth negative

- Best Case: Free cash flow drops quite a bit in year 1, but makes a slow recovery as management withdraws from making acquisitions, and focuses on the Core Business.

- I have assumed an equal probability weight for all 3 scenarios. I believe that the presence of an activist investor, and managements own stated objective in the last earnings call to rationalise the cost structure and stabilise cash flows, merits a more optimist weight, but I chose to be conservative.

Yahoo’s CORE Business – BASE CASE

Notes & Assumptions for BASE CASE

- Adjusted EBITDA, free cash flow, tax, and capex is based on Yahoo Inc’s financials.

- The scenario assumes nil revenues from both the Alibaba license fee (TILPA) which has now expired, and from gain on sale of patents.

- Royalties from Yahoo Japan are projected to be stable at $262m each year; this is consistent with pervious years, and Yahoo Japan Royalties have been highly stable throughout.

- I have assumed that Yahoo’s Core Business EBITDA will drop by 25% in FY16, 20% in FY17, 10% in FY18, 5% in FY19, and stabilise thereafter.

- Taxes are assumed to be stable at 16%; this was the average effective tax rate between FY12 – FY14 when the business was tax paying.

- I have assumed that the business will stop throwing money behind new acquisition, and focus on the Core Business. For Capex, I have assumed that this will drop by 10% for FY16, 20% for FY17, 25% between FY18 to FY20, and stabilise thereafter. Majority of the capex in the base years have been a result of acquisitions; therefore, the projected drop in capex is consistent with the assumption that the company stops making significant new acquisitions.

- I have assumed a WACC of 8.5%, calculated using the company’s capital structure, and per CAPM.

- The value of employee share options have been calculated using Black Scholes formula. The source data on number of options, weighted average strike price, and volatility is from company financials.

- In conclusion, my estimate of intrinsic value for the BASE CASE is $2.3bln

Yahoo’s

CORE BUSINESS – WORST CASE

Notes & Assumptions for BASE CASE

- Adjusted EBITDA, free cash flow, tax, and capex is based on Yahoo Inc’s financials.

- The scenario assumes nil revenues from both the Alibaba license fee (TILPA) which has now expired, and from gain on sale of patents.

- Royalties from Yahoo Japan are projected to be stable at $262m each year; this is consistent with pervious years, and Yahoo Japan Royalties have been highly stable throughout.

- I have assumed that Yahoo’s Core Business EBITDA will drop by 50% in FY16, 30% in FY17, 15% in FY18, 10% in FY19, and stabilise thereafter.

- Taxes are assumed to be stable at 16%; this was the average effective tax rate between FY12 – FY14 when the business was tax paying.

- I have assumed that the business will continue to leak money on capex. For Capex, I have assumed that this will average the rate in last 4 years for FY16, drop by 10% between FY17 – FY20, and stabilise thereafter.

- I have assumed a WACC of 8.5%, calculated using the company’s capital structure, and per CAPM.

- The value of employee share options have been calculated using Black Scholes formula. The source data on number of options, weighted average strike price, and volatility is from company financials.

- In conclusion, my estimate of intrinsic value for the WORST CASE is that the business has no value.

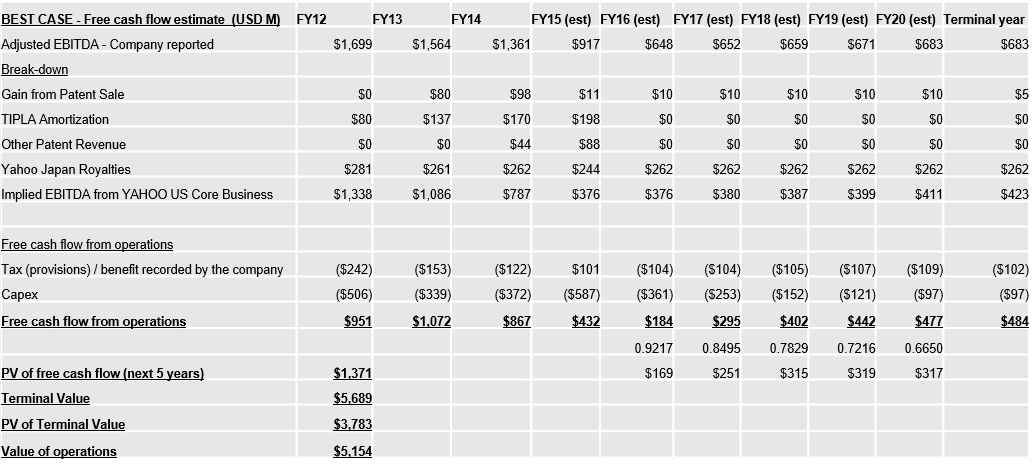

Yahoo’s CORE BUSINESS – BEST CASE

Notes & Assumptions for BASE CASE

- Adjusted EBITDA, free cash flow, tax, and capex is based on Yahoo Inc’s financials.

- The scenario assumes nil revenues from the Alibaba license fee (TILPA) which has now expired, and $10m from gain on sale of patents over the next 5 years, and $5m thereafter. The average yearly revenues from gain on sale of patents have been $63m in the last 3 years.

- Royalties from Yahoo Japan are projected to be stable at $262m each year; this is consistent with pervious years, and Yahoo Japan Royalties have been highly stable throughout.

- I have assumed that Yahoo’s Core Business EBITDA will remain stable in FY16, and grow by: 1% in FY17, 2% in FY18, 3% in FY19 and future years.

- Taxes are assumed to be stable at 16%; this was the average effective tax rate between FY12 – FY14 when the business was tax paying.

- I have assumed that the business will stop throwing money behind new acquisition, and focus on the Core Business. For Capex, I have assumed that this will drop by 20% for FY16, 30% for FY17, 40% for FY18, 20% for FY19 and FY20, and stabilise thereafter. Majority of the capex in the base years have been a result of acquisitions; therefore, the projected drop in capex is consistent with the assumption that the company stops making significant new acquisitions.

- I have assumed a WACC of 8.5%, calculated using the company’s capital structure, and per CAPM.

- The value of employee share options have been calculated using Black Scholes formula. The source data on number of options, weighted average strike price, and volatility is from company financials.

- In conclusion, my estimate of intrinsic value for the WORST CASE is that the business has no value.