It is likely to be a bumpy ride.

The Company

Enterprise Inns is a UK based

company which operates a leased and tenanted pub model. The company owned 5,069

pubs as at September 2015 within an overall market of approximately 47,000

pubs. Majority of its pubs (c.95%) are leased to the tenants (who are commonly

referred to as Publican) under the so called – ‘beer tie’ or ‘tie’.

Source: Enterprise Inns Annual report

As can be seen from the

diagram above, under the ‘tie’:

- the Publican must

buy all their beer, and some other supplies from the PubCo (typically at a

higher rate than the wholesale price). This is commonly referred to as the ‘wet

rent’;

- the Publican

must also pay rent to the PubCo. The rent is typically arranged at 50% of the

projected profits at the start of the lease, with generally an upward only rent

review provision;

- in addition

to the above, a percentage of income from amusement with prizes machines (AWPs)

– you may have dabbled in fruit and quiz machines in your time at the Pub –

goes to the PubCo.

The

rationale behind the ‘tie’ is that it offers the Publican an easy access to the

business – they don’t need the capital to buy/own a Pub to get started, and the

PubCo can use its economies of scale to buy other services in the cheap for the Publican

(e.g. insurance, satellite television, fittings/maintenance etc.). Also, the

model is supposed to have a better alignment of interest between the PubCo and

its Publican –PubCo charges a lower fixed rent, and makes most of its money via

drink sales; ergo, when the Publican does well, the PubCo does well, and

vice-versa.

There has been a huge amount of criticism

of the ‘tie’ of late, resulting in the UK bringing in new regulations – which

will take effect from March 2016 – making it mandatory for the PubCos to offer

its Publican’s and option to go ‘free of tie’ at the point of lease renewals

(more on this later).

Enterprise

Inns also operates 213 Pubs ‘free of tie’ where it simply collects rents; and,

it currently has 35 Pubs that it manages directly. Both the ‘free of tie’ and

‘managed’ pub numbers are set to rise significantly over the next 5 years, with

the ‘tie’ Pub numbers set to fall.

The stock

The chart

below show’s how the stock has performed over the last 5 years

As can be

seen, the stock hasn’t done anything for someone who has stayed the

journey. That said, if one had purchased the stock towards the end of 2011 or in early 2012 (when it touched the lows of 28p), they could have had a 3x-4x return. The question

today is where is the stock now? In particular, is it a value opportunity?

Coming back

to point, the stock currently trades at 103p; this equates to PE multiple

of 5.3 and EV/EBITDA multiple of 9.8 (based TTM). The sector typically trades

at a EV/EBITDA multiple of between 9X – 11X. On that basis, the shares don’t

seem to be trading at a significant discount.

The other

point worth noting is the discount to NAV, which currently stands at over 60%. The

NAV per share as at Sep15 stood at 270p versus the share price today of 103p.

This is all the more interesting because the company undertook an external

valuation of almost all of its Pubs recently underpinning the 270p per share

NAV (previously the company did most of the valuation in-house). If one assumes

– as one should – that valuation reflects

the current and future rent and other income streams expected to be generated

by each property, capitalised using an appropriate multiple, then the market is

mispricing the shares. But is it?

Before we

get into answering that question, it is worth nothing the trading history of

the stock compared to NAV

Source: Enterprise Inns 2013 Results presentation

As can be

seen in the chart above, the stock was trading at a significant premium to NAV

until the property markets tanked in 2008. Since then, the discount to NAV

narrowed from 88% to 49% between 2011 and 2013, but it has turned up again and

currently stands at just over 60%.

In my

opinion, the pre-2008 premium to NAV was clearly not justified; but at the same

time, is the current discount to NAV justified?

The only way

to answer that question is by determining the intrinsic value for the stock.

But before we do that, it is helpful to take stock of three very important

factors which have a material impact in this exercise.

1. The state of pubs

‘When you have

lost your inns, drown your empty selves, for you will have lost the last of

England.’

Hilaire

Belloc (1912)

If the famous Anglo-French writer and historian, Hilarie Belloc, got to

see us today, he will likely declare that the time for the people of England to

drown their empty selves may be approaching soon.

The future

of pubs in the UK has been high on the political agenda for a few years now.

Depending on source, anywhere between 20 and 30 pubs are closing shop at present.

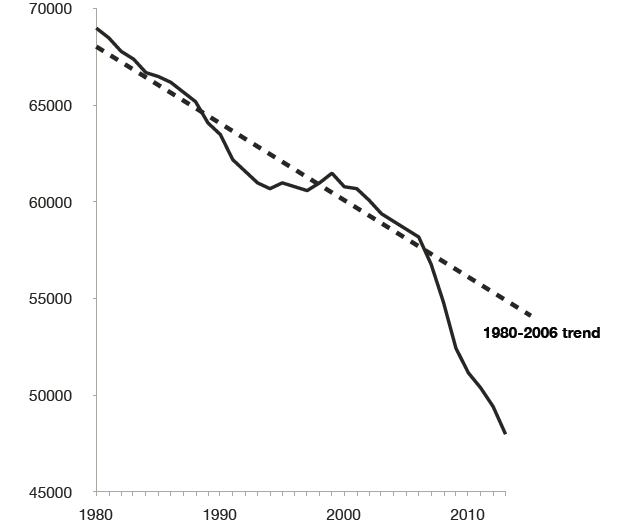

In 1980 there were c70,000 pubs in the UK; the number now stands at c47,000.

As can be seen from the graph above, the closure rate has been particularly alarming since

the 2008 recession. The number of pubs plummeted from 58,200 in 2006

to 48,000 in 2013, a drop of 18 per cent in just seven years (BBPA). The peak

in pub closures came in 2009, with 52 pubs shutting down each week, but pubs

were still closing at a rate of 20-30 a week in mid-2014.

People's drinking habits have changed

There is no

doubting the fact that people’s drinking habits have changed over the years. There

is more choices today – from cheap supermarket beer, to quality wines from all

across the globe. Also, the coffee shop is partly acting as the social hub for

the discerning professional. In addition, things like the smoking ban (smokers

on average tend to consume more alcohol than non-smokers), VAT, and alcohol

duties have not helped. And, there is the small matter of the explosion in home

entertainment (internet and satellite TV), which has domesticated a lot of the

men folks. All these factors combined has meant that people don’t frequent the

Pubs as they used to.

The following two chart’s capture this point nicely:

Beer vs Coffee

Source: FT

Per capita alcohol consumption (litres)

Smoking ban and Pub numbers

Enterprise,

like all other Pub owners, has not been immune to this change. At its height,

Enterprise had over 9,000 pubs. Since 2008, the company has sold many

pubs, with 5,069 remaining at the end of September 2015.

That said, Pubs are not going to disappear from

the UK. There has been a massive shake up, but the process will most likely

lead to profitable pubs. Pubs that will remain, will be evolved, and profitable

– already we are seeing pubs offering food and variety.

A number of stakeholders interviewed by

London Economics for a report to the Department for Business, Innovation and

skills on the impact of policy changes (see Incoming regulation below noted

that a sustainable number of pubs in the UK would be 45,000. We are almost at

that level now.

2. Incoming regulation – Market Rent

Only (MRO) option

In a debate

on Pubs and the ‘Beer tie’ in the UK parliament on 21 January 2014, the then

Secretary of State, Vince Cable, addressed the question of whether tied pubs

were more vulnerable to going out of business than independent or free-of-tie

pubs. After saying that there was no clear evidence to suggest that tied pubs

were more vulnerable to closure than free-of-tie pubs, Mr Cable went on to say:

This is not fundamentally an argument about

pub closures; it is essentially about the unfairness of and inequalities in the

relationship … To us, the essential point is best captured in the work done by

CAMRA that suggests that 57% of tied tenants earn less than £10,000 a year. If

we apply that to 35-hour week, 48 weeks a year, we are talking about less than

£6 an hour, which means that people are working for considerably less than the

minimum wage. Since many work much longer hours, that means that this is a very

low-paid industry. Many publicans are struggling. In contrast, only 25% of

those who are free of tie are on at the same income level. There is a striking

disparity, which is at the heart of the question.

The above quote from Mr Cable, in essence, captures the rationale

behind the new regulations – MRO option – being introduced from May 2016. Broadly, the Market Rent

Only (MRO) option allows the Publican to go free-of-tie, effectively ending the

need to buy beer from the PubCo (with the exception of buildings’ insurance).

The PubCo would effectively cease to have any direct involvement in the trading

operations and the PubCo – Publican relationship would be that of a pure

landlord and tenant. Under the MRO the Publican can request the free-of-tie

option either at rent review time or at lease renewal, after the law comes into

effect in May 2016. The MRO only applies to PubCo which own over 500 pubs –

broadly, the affected companies will be Enterprise, Punch, Admiral, Green King,

Star, and Marstons. The total number of Pubs that will be affected is expected

to be approximately 13,000; of which Enterprise has 4,821 – by far the largest

share (Punch comes next).

There is no question of the fact that MRO is a negative for the PubCos.

Its effect will be a transfer of wealth from the PubCos to the Publican –

currently, a larger share of the wealth is being captured by the PubCo under

the ‘tie’; by allowing the Publican to buy his beer in the open market, the MRO

will erode the margin that the PubCo gets to keep as the middle man.

For enterprise, there are two important points to note:

-

Its portfolio

will look fundamentally different in 5 year’ time, by which time almost all of

its tied pubs should have had a rent review, with the Publican having selected

whether or not to go free-of-tie. The company anticipates 200 MRO events in

2016, and some 600 such events per year thereafter. Therefore, by the end of

2020, it could find itself owning no Pubs under ‘tie’, if all of its tied

Publicans chose the free-of-tie option under the MRO. Management is spending a

lot of effort trying to convince its Publicans of the benefits of staying with

the ‘tie’, however, even Management expects a significantly reduced portfolio

of tied pubs. Broadly, of the c4200 pubs at the end of Sep 2020, Management

expects that c2400 will be ‘tied’.

-

With little ‘base

rate’ data, it is difficult to calculate the precise wealth transfer that will

result from the MRO. But we can make a reasonable start with the data that is

available. Based on the data available from the existing 213 free-of-tie pubs I

we know that the rents from the free-of-tie pubs is c60k per annum. And, analysing

the last six years financials, we can calculate the gross profit per tied pub

(revenue less COGS) as c72k per pub. Therefore, based on current best

estimates, we get a c12k per pub of gross profit reduction when moving from a

‘tie’ to ‘free-of-tie’.

In addition, Enterprise will not spend the same amount it currently

spends in capex and improvements if a pub is ‘free-of-tie’. I have assumed a

40% drop in capex for ‘free-of-tie’ pubs.

3. The Debt

Enterprise came close to insolvency during the

financial crisis, thanks mainly to its debt level which stood at 8 times EBITDA

in 2010. Enterprise’s net debt is now down to £2.3bn, but still stands at very

high 7.8 times EBITDA. From a Loan-to-Value perspective, the property assets

are valued at £3.7bn – giving a LTV of 62%.

The chief risks on the debt are:

Liquidity risk: The Company has on average

required c176m per year of interest and other payments over the last 5 years.

This eats into substantial part of its free cash flow, leaving little freedom

in operations.

Refinancing risk: The Company has c350m of debt

that needs to be refinance in 2018; and a total of c1.5bln that needs to be

refinanced in the next 10 years. This is significant amount of debt to

refinance.

Property values: The property portfolio has been

falling steadily over the years – both due to sales, and due to write-downs. In

the year ending September 2015, the company took a write-down of c121m to its

property portfolio. The risk is that the property portfolio falls at a faster

rate to debt, this risk is compounded by the significant change that is coming

due to the MRO.

Management’s new strategy

Driven by

the MRO, Enterprise, in May 2015, announced a radical change to the shape of

its business. The key points coming out of the revised strategy are:

-

plans to

sell c1000 pubs over the next 5 years;

-

plans to

significantly increase the number of pubs under its own management, from the

current 35 to c800 in the next 5 years; and,

-

at the end

of 5 years, Enterprise expects to have c2400 pubs under the ‘tie’ and c1000

pubs under ‘free-of-tie’. In addition, it plans to spin-off the ‘free-of-tie’

portfolio as a REIT.

The below

graph shows the portfolio as it stands currently

Source: Enterprise Inns preliminary presentation September 2015

The below

graph shows the portfolio as predicted at September 2020, once the new strategy

has been implemented

Having run

the numbers, I do believe that the proposed strategy is the best option in

front of the company. However, it comes with significant execution risks. In

particular, the following challenges exist:

-

a

significant proportion of the returns are projected from converting ‘tied’ pubs

to managed house. Managed houses could bring with them significant volatility

due to higher operational gearing inherent in it. Moreover, executing 800 managed

house formats – requiring branding, tie-ups, capex etc. - will be a significant

challenge.

-

although

the group should have sufficient cash flow to execute the plan based on current

forecast from trade and proceeds from sale of pubs, there will be little breathing room. Any change to forecast

– be it at the income level or with capex, could present problems.

Intrinsic value estimate

Given the

significant uncertainty due to the MRO, the degree of added risk due to debt,

and the execution risk under the new strategic plan, the range of possible

outcomes at this stage are many. With this in mind, I have calculated the intrinsic

value using a range of possible outcomes which I believe best capture the

uncertainty as we stand today.

I have

used management’s predicted portfolio mix at the end of September 2020 as the

starting point –management predict a portfolio consisting of 57% tied pubs, 24%

free-of-tie pubs, and 19% managed pubs, in a total portfolio of 4200 pubs. This

to me is the best case scenario. Using this as a base, I have added on a number

of different scenario for the portfolio mix as at September 2020 and calculated

the value of the stock for each scenario. My overall estimate is an average of

the stock price for all the scenarios. Considering where we are today, I

believe that these scenarios capture the range of possible outcomes

appropriately. Obviously, as things evolve with the portfolio, I will be better

able to adjust my range of possible outcomes. The below table summarizes the

outcome:

You are

welcome to review and play around with the detailed spreadsheet by downloading it

here - https://drive.google.com/file/d/0B19r4lez4O3tMUVZY3BqMmhIWjQ/view?usp=sharing

The

valuation summary shows my predicted share price for 35 scenarios – for 6

different pub mixes between tied, free of tie, and managed, and for 5 different

total number of pubs at September 2020.

If

management execute on their current strategy to the dot, and everything works

out perfectly, then the shares are worth 133.87p (the top right hand corner of the

summary). However, average price I get for the range of outcomes is 67.29p.

Therefore, in my opinion, as a value investor, the stock is overpriced given

the risk. Although it is not a buy for me at current levels, I will continue to

monitor the situation as it evolves.

Afterword

Enterprise

may have let down its shareholders, but it has certainly been good to its debt

holders. The company pays an average interest rate of 6.3% on its £2.4bln of

debt – a combination of bank debt (£75m), convertible bond (£97m), a large

trance of corporate bond (£1.1bln), and securitized bond (£1.1bln). Back in the

summer of 2011, its 2018 corporate bonds traded at mid-seventies, pushing the

yield to 12%. The buyers then ended up making a decent turn with much lower

risk than in the equity.

The bonds

seem fairly priced now, but they are certainly worth a watch. Any distress, and

it might be a better idea to enter into the bonds, than the equity.

By the

way, the convertible bond doesn’t seem that much of a value for money at

present. It only pays a coupon of 3.5% (compared to the bonds which average

6.5%), and the conversion price is at £1.91 a share at September 2020. Based on

current predictions, I can’t see much value in this, unless it is trading at a

significant discount.