In mid-November last year I wrote about the situation at Yahoo I concluded that Yahoo should give up its planned spin-off of Alibaba stake, and seek to sell its core US business instead. My analysis showed that the stock should be worth at least $47-$48 in this scenario.

Under pressure from activists, by the end of last year, Yahoo announced its withdrawal of the Alibaba spin-off. Whilst confirming that it will be open to offers for its core US business, Yahoo has announced a new plan to spin-off its core US business and its 35% stake in Yahoo Japan, leaving Alibaba stake in the legacy structure.

(In $M)

The current valuation of Yahoo implies a combination nil or negligible value for Yahoo’s core US business, combined with a material tax liability on the proposed spin-off plan.

As if often the case, high uncertainty situations are misunderstood as high risk, offering a value opportunity. In my view the stock is mis-priced and is worth $46 - $48, offering a 1.6X – 1.7X return over the next 8-12 month.

As if often the case, high uncertainty situations are misunderstood as high risk, offering a value opportunity. In my view the stock is mis-priced and is worth $46 - $48, offering a 1.6X – 1.7X return over the next 8-12 month.

The catalyst event will be either the sale of Yahoo’s core business or the spin-off of its core business and Yahoo Japan stake. In my opinion, the sale of the core business offers the best outcome and one which Yahoo may eventually implement pursuant to pressure from activists.

Valuation summary

In order to value Yahoo, one needs to determine the intrinsic value of its component parts:

In order to value Yahoo, one needs to determine the intrinsic value of its component parts:

- Yahoo’s core US business;

- 15.4% Alibaba stake;

- 35.5% Yahoo Japan stake; and,

- estimated tax liability for the following scenarios – 1) tax on sale of its core US business, and, 2) tax on spin-off of its core US business and Yahoo Japan stake.

- In summary:

- I value Yahoo’s share of Alibaba @ $30 billion; Yahoo’s share of Yahoo Japan @ $7.8 billion and, Yahoo’s core US business @ $3.9 billion

- My estimated tax liability for the spin-off scenario is $3.6bln, and for the sale of core business is $1.4bln

- My intrinsic per share value is $46 under the spin-off scenario, and $48.4 under the sale of core business scenario

- Compared to the 5 Feb 2016 closing share price of $27.97, the shares trade at a 39% - 42% discount to intrinsic value

Detailed

valuation

Yahoo’s

core US business

- Profitability in Yahoo’s core Search and Display advertising business has dramatically decrease since the new management was put in place in 2012. This is despite the fact that over this time Yahoo spent close to $6 billion in acquisitions and product development costs. Yahoo’s LTM core business Adjusted EBITDA has declined by 57% since 2012.

- Despite the declining profitability trend, Yahoo’s core business will be of significant interest of buyers given the number of unique users, significant search revenue and income, popularity of many of Yahoo’s display properties, and valuable real estate and intellectual property.

- Under new ownership, without the significant capital spend as seen over the past 3 years on unprofitable and value destructive acquisition, Yahoo core business should return to profitability.

- I have valued the core business under both a base case and a best case basis, and arrived at a of value of $3.9 billion.

The detailed valuation for the

base case and best case is shown below, along with my assumptions.

Assumption

1. The scenario

assumes nil revenues from both the Alibaba license fee (TILPA) which has

now expired, and from sale of patents.

2. Royalties from

Yahoo Japan are projected to be stable at $266m each year; this is

consistent with prior years.

3. Yahoo’s core business

EBITDA is assumed to drop by 25% in FY16, 20% in FY17, 10% in FY18, 5% in

FY19, and stabilise thereafter.

4. Taxes are assumed

to be stable at 16%; this was the average effective tax rate between FY12

– FY14 when the business was tax paying.

5. The business will stop throwing money behind new acquisition, and

focus on the core search and display advertising business. Capex is

assumed to drop by 10% for FY16, 20% for FY17, 25% between FY18 to FY20,

and stabilise thereafter. Majority of the capex in the base years have

been a result of acquisitions; therefore, the projected drop in capex is

consistent with the assumption that the company stops making significant

new acquisitions.

6. I have assumed a

WACC of 8.5%, calculated using the company’s capital structure.

7. In conclusion, my

estimate of intrinsic value for the BASE CASE is $2.4bln

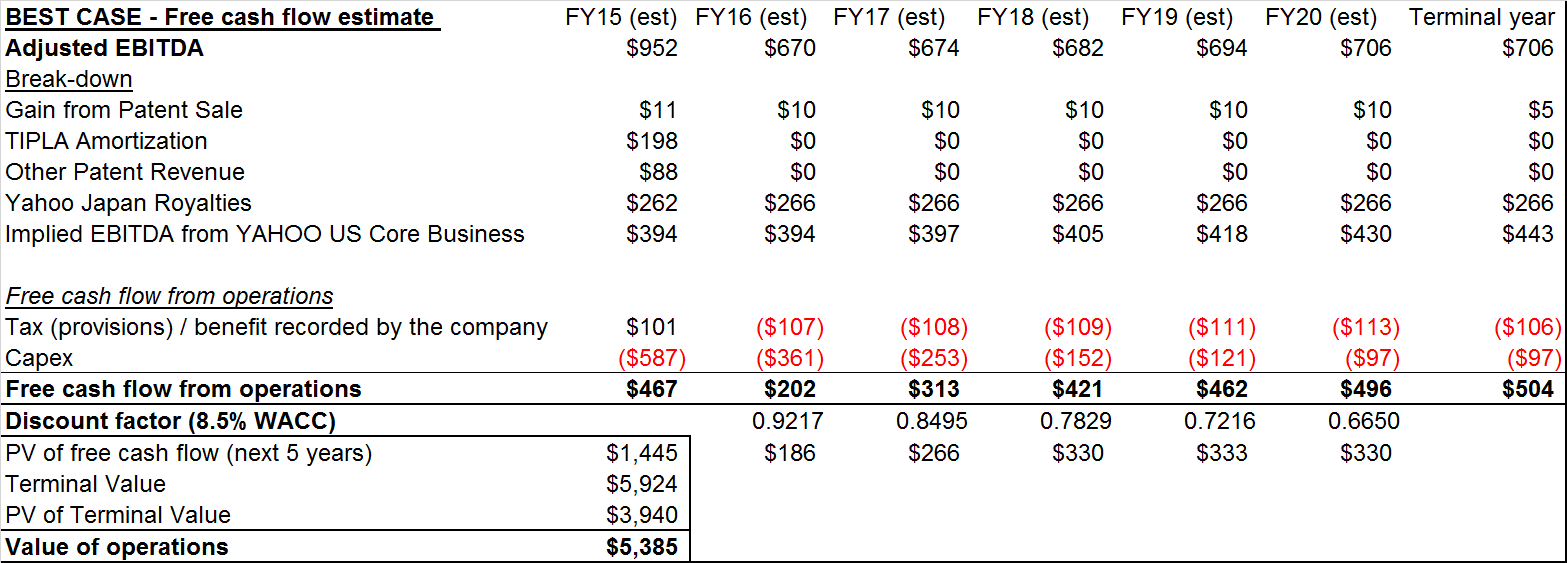

Assumptions

1. The scenario assumes nil

revenues from the Alibaba license fee (TILPA) which has now expired, and $10m

from gain on sale of patents over the next 5 years, and $5m thereafter. The

average yearly revenues from gain on sale of patents have been $63m over the

last 3 years.

2. Royalties from Yahoo Japan are

projected to be stable at $266m each year; this is consistent with prior years,

and Yahoo Japan Royalties have been highly stable throughout.

3. Yahoo’s

Core Business EBITDA will drop to $670m in FY16, and grow by: 1% in FY17, 2% in

FY18, 3% in FY19 and future years.

4. Taxes are assumed to be stable

at 16%; this was the average effective tax rate between FY12 – FY14 when the

business was tax paying.

5. The

business will stop throwing money behind new acquisition, and focus on the Core

Business. For Capex, I have assumed that this will drop by 20% for FY16, 30%

for FY17, 40% for FY18, 20% for FY19 and FY20, and stabilise thereafter.

Majority of the capex in the base years have been a result of acquisitions;

therefore, the projected drop in capex is consistent with the assumption that the

company stops making significant new acquisitions.

6. WACC of 8.5%,

calculated using the company’s capital structure.

7. In conclusion, my

estimate of intrinsic value for the BEST CASE is $5.4bln.

Alibaba

value

-

My estimate of the intrinsic value per share

for Alibaba was just over $80 in November last year, and my estimate today is

roughly the same. Although the stock price has been highly volatile lately, and

today trades at a low of $62.64, I believe this is more to do with the general

volatility in the equity markets, particularly China.

Alibaba continues to be a great business with some quality traits:

Alibaba continues to be a great business with some quality traits:

- It is a highly profitable business with EBIT margins of over 40% and free cash flow at 40%-50% of revenue (this is significantly better than other technology darlings of the stock market like Alphabet, Apple, Facebook, Amazon, Ebay)

- It has roughly 367m buyers using its e-commerce platforms in China, equating to roughly 20% of the Chinese market. This gives it a very strong a durable moat.

- E-commerce sales in China only represent 10% of the retail sales, offering significant growth prospects. Alibaba is set-up perfectly to tap into this and a lot of growth is yet to come.

- It has experienced revenue growth of just under 30% in each of the last 5 years, and this trend is likely to continue for the foreseeable future as China transforms to a more consumption oriented economy.

Yahoo

Japan

-

There is not much difference between my

estimate of Yahoo Japan’s intrinsic value - @$3.94 and the current share price

@ $3.9. I think the stock is fairly priced.

My DCF valuation for Yahoo Japan is shown

below.

Tax

risk

There are two scenario which need to be modelled for tax:

1. Where

Yahoo spin’s off its core business along with Yahoo Japan stake, as currently

intended

2. Where

Yahoo’s core business is sold to a prospective buyer

Although, it may be possible

under the US tax code to spin-off Yahoo core and Yahoo Japan in a tax free

manner, I have assumed that this transaction will be taxed. This is prudent

given the history with respect to the Alibaba spin-off, and the changing tax

landscape with respect to tax free spin-offs.

The one area

of risk in my valuation is my conclusion that Alibaba stock is worth $80 vs the

current price of $62.64. However, even using the $62.84 value for the Alibaba

stock, the intrinsic value for the Yahoo stock should be $40 per share. At the current

price of $27.97, this still offers a decent margin of safety.

No comments:

Post a Comment